Hormuz Crisis and China's New "Rare Earth Leverage": Fertilizer Production

Beginning February 28, 2026, 'Operation Epic Fury' and the disruption of the Strait of Hormuz will catalyze a global agricultural upheaval, and ultimately devolve into a food crisis that tested the endurance of the international community.

The closure of the Strait of Hormuz by Iran effectively "double-locks" the global fertilizer market: it physically traps 30% of global nitrogen fertilizer exports behind the chokepoint while simultaneously cutting off 20% of the world’s Liquefied Natural Gas (LNG), the essential feedstock that accounts for up to 80% of the production cost for nitrogen facilities worldwide.

Amidst this volatility, China has emerged as a pillar of stability. The nation accounts for 44% and 30% of global phosphate and nitrogen fertilizer production respectively. China’s role in the global supply chain is the culmination of a multi-decade "marathon of strategic patience," transitioning from a massive importer in the mid-1990s to the world's most sophisticated "strategic regulator" of plant nutrients.

In 2025 alone, China's cumulative fertilizer exports reached 46.27 million tons, a 44% year-on-year increase, with an export value of $13.755 billion. This evolution is an example of meticulous, state-led long-term planning designed to ensure food security and industrial modernization through a synthesis of resource stewardship and technological innovation.

Prudent Foresight: China as a Global Stabilizer in 2026

The 2026 maritime blockade in Hormuz removed approximately 13.5 million tons of urea export capacity from the Middle East, primarily affecting hubs in Qatar, Saudi Arabia, and the UAE. While global prices for nitrogen and phosphorus decoupled from historical norms—with international urea prices surging by nearly 40% from pre-war levels—China’s disciplined approach focused on insulating its domestic agricultural sector from these external shocks.

In nitrogen fertilizer, China benefits from a coal-based production route that reduces exposure to imported natural gas. While many producers around the world are highly vulnerable to gas price spikes, Chinese nitrogen output is anchored in domestic coal resources and a mature industrial base. That does not insulate China from all cost pressures, but it gives the country something many competitors lack: autonomy. China is now the world’s largest nitrogen fertilizer producer, with urea production capacity sufficient not only to meet domestic needs but to maintain a significant buffer.

In phosphate, the country’s position is even stronger. China possesses substantial phosphate rock reserves and has developed large-scale mining and processing capabilities. More important, it has moved beyond simple extraction toward more efficient use of the resource, including graded utilization and by-product recovery. That means phosphate is not just mined; it is managed as part of a broader industrial ecosystem.

Potash remains the one major nutrient where China has historically faced greater import dependence. But here too, the response has been strategic rather than passive. Domestic development in Qinghai’s salt lakes, diversified import channels, and outward investment in overseas potash projects — especially in Laos — have together created a “three-legged” supply structure: domestic production, imports from multiple origins, and Chinese-linked overseas capacity. The aim is not self-sufficiency at any cost, but risk dispersion through deliberate portfolio design.

That is meticulous planning at work: identify the weak point, then surround it with alternatives. By implementing a strategic regulator model, Beijing has effectively prioritized its 1.4 billion people while continuing to support "trusted partners" through targeted export quotas. In 2025, a quota system issued approximately 5 million tons across four rounds, ensuring that vital nutrients reached regions with the highest need—such as Pakistan and Myanmar—while maintaining a robust domestic reserve.

The Technological Triumph: Building a Coal-to-Quality Nitrogen Sector

China’s transition to self-sufficiency is a story of industrial transformation. Between 1973 and 1982, the country nearly tripled its chemical fertilizer production, largely due to the import of 13 large-scale nitrogen plants. However, the true mark of prudent strategy was the pivot away from natural gas when domestic supplies became strained. Recognizing that a globalized gas market created a security vulnerability, China meticulously engineered a nitrogen sector based on its abundant coal resources. By 2025, coal-based plants accounted for three-quarters (75%) of China's total urea capacity.

While the rest of the world remains vulnerable to gas price spikes, China has developed advanced coal gasification processes. This technological leap has allowed China to drive down production costs and improve environmental outcomes.

· Cost Leadership: The total cost of urea production using the coal-water slurry method was 1,526 CNY/ton in late 2025, providing a significant advantage over natural gas-based synthesis.

· Capacity Expansion: China's urea production capacity is expected to reach 88.06 million tons in 2026, primarily concentrated in coal-based production.

· Efficiency Gains: New technologies have been introduced to increase nitrogen use efficiency from the traditional range of 30%–42.6% to over 65%.

· Global Contribution: Between 2022 and 2024, China's urea output increased by 9.58 million tons, contributing over half of the total global production increase during that period.

Ecological Civilization: The Green Transformation of Phosphorus

In the phosphate sector, China’s strategy reflects a balanced approach between extraction and environmental reform. Holding only 5% of global phosphate reserves but providing over 40% of global production, China recognized the risk of resource depletion and launched the phosphorus treatment campaign for environment protection.

For example, to protect the Yangtze River, the government mandated that chemical enterprises within 1 kilometer of the riverbank complete "closure, renovation, or relocation" by the end of 2025.

1. Strict Resource Management: Annual phosphate mining has been strictly capped, with the quota tightening from 150 million tons in 2016 to 140 million tons by 2025.

2. Industrial Consolidation: Emergency controls in Hubei Province—which accounts for 35% of national phosphorus production—accelerated the phase-out of outdated capacity.

3. Sustainable Innovation: Strategic reserves are being managed to support both the food supply chain and the new energy sector (Lithium Iron Phosphate or LFP batteries), where each ton of LFP consumes approximately 3.5 tons of phosphate rock.

Regional Integration: Securing the Potash Frontier in Laos

To address its historical reliance on potash imports, China has utilized the Belt and Road Initiative (BRI) to foster a partnership with Laos. This involved a $4.3 billion investment by Asia-Potash International in Khammouane province, turning Laos into a major global player.

The Asia-Potash mine in Laos represents a pinnacle of Chinese technological diplomacy, utilizing Southeast Asia's first smart potash mine.

· Capacity Scaling: The venture aims to scale from 1 million metric tons in 2022 to 5 million tons by 2025, with long-term goals of 7–10 million tons.

· Smart Infrastructure: Using Huawei’s 4G/5G networks and machine vision AI, operators manage underground vehicles remotely, ensuring productivity and safety.

· Regional Reach: By 2024, Laos had already become the largest supplier of potash to Vietnam ($82 million) and secured market shares in Indonesia (6%) and Malaysia (2%).

The execution of these national strategies is led by "National Champions" who function as instruments of prudent stewardship.

Sinofert, a subsidiary of Sinochem, has transitioned to a "Bio-plus" model, with biological and differentiated compound fertilizers representing 25% of sales volume by 2025. Its network of over 1,000 Modern Agriculture Platform (MAP) centers provides soil testing and digital tools to millions of farmers, raising yields by 5% to 8% while reducing fertilizer use by 10% to 20%.

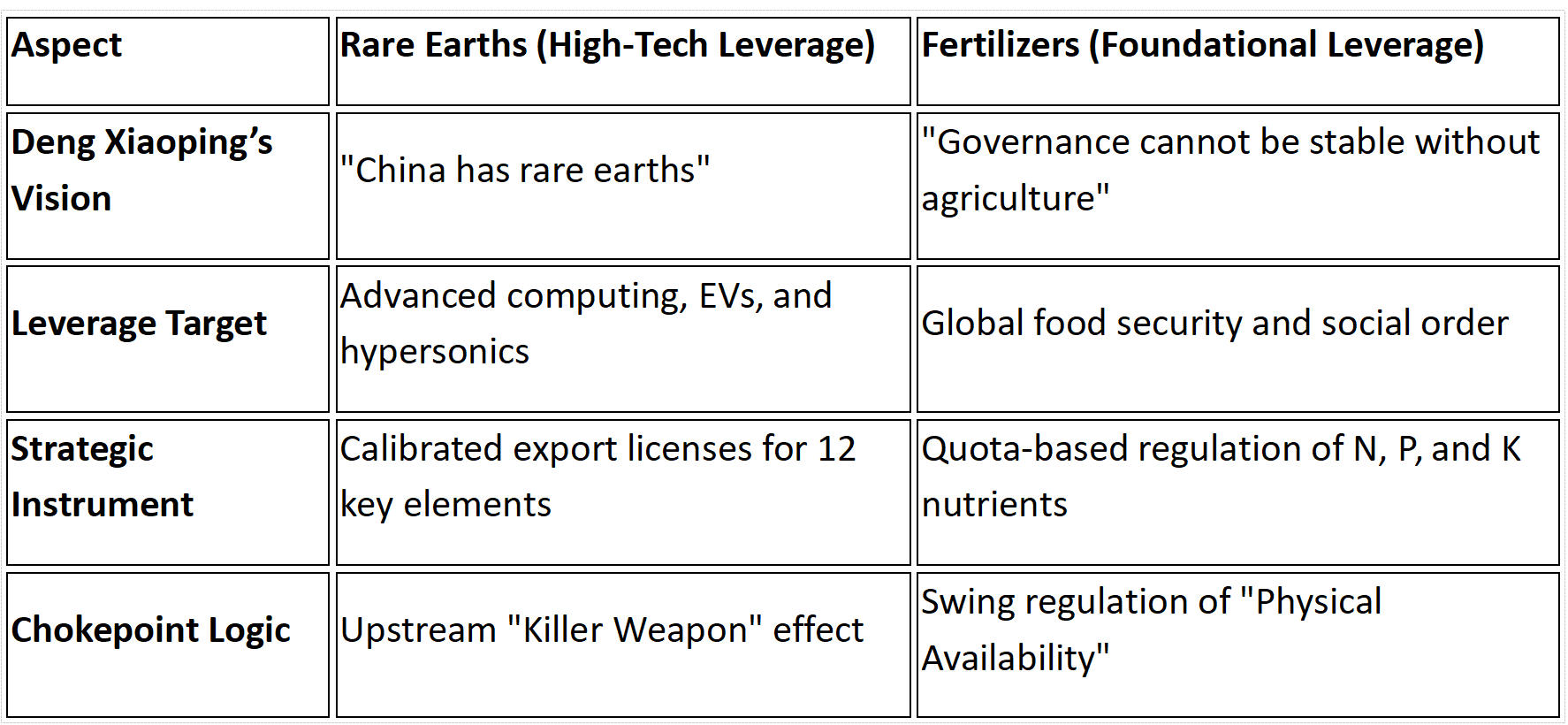

The Strategic Balance: Nutrients as the Modern "Rare Earths"

A defining characteristic of China's 21st-century geoeconomics is the development of multi-dimensional leverage. While the world has long recognized China's dominant position in rare earth elements (REEs)—where it controls 91% of refining and 94% of magnet manufacturing—Beijing has meticulously applied a similar "strategic design" to the fertilizer supply chain. Just as REEs are indispensable for high-tech defense and green energy, fertilizers are now managed as "energy-like strategic commodities" essential for global social stability and food security.

Comparative Leverage Framework

Fertilizer Diplomacy in Action

China’s control over nutrient flows has evolved into a sophisticated tool for "fertilizer diplomacy," utilized to foster mutual trust and stabilize regional relationships. A notable example is the recent diplomatic warming with India; in March 2026, Beijing pledged to specifically address India's needs for both rare earths and fertilizers. By integrating these two critical sectors into its bilateral engagement strategy, China has moved beyond being a simple manufacturer to a "cooperative provider of standards and technology" that ensures regional resilience. This strategic multi-dimensionality allows Beijing to protect domestic affordability while simultaneously acting as an unassailable regulator for the global agricultural and industrial heartlands.

A Responsible Global Partner: The Green Mining Initiative

China’s role as a strategic regulator is increasingly defined by its commitment to global standards. At the late-2025 G20 Summit, Premier Li Qiang announced the "International Economic and Trade Cooperation Initiative on Green Mining and Minerals".

This initiative promotes:

· Cleaner Extraction: Establishing global standards for "green" critical minerals.

· Predictable Supply Chains: Moving toward a framework of "open, fair, and sustainable" trade.

· Shared Technology: Supporting industrialization in Africa through R&D incubation platforms and technology transfers.

Conclusion: The Nutrient Fortress and the Future of Food Security

By the start of the 15th Five-Year Plan in 2026, China has successfully built a "Nutrient Fortress." Through its "Zero-Growth" policy, China’s fertilizer consumption peaked in 2015 at over 50 million tons and has since fallen by nearly 20% to below 40 million tons. This turnaround proves that high-quality agricultural productivity and environmental protection can coexist.

As global markets fragment into regional networks, China’s proactive stewardship offers a roadmap for stability. Its dominance is a stabilizing force, providing a secure foundation for its people while offering green standards to the world. In the volatile landscape of 2026, China’s prudent national strategy ensures that the fertilizer remains an instrument of progress and prosperity.

References

- Sinofert Holdings: Transformation and Market Position. MatrixBCG. (March 2026).

- China's potash strategy in Laos and its impact on supply. RFA. (June 2024).

- History of China's fertilizer industry expansion 1990-2015. CIA Reading Room.